Top CD rates today: Top rates remain competitive — April 29, 2024

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

BLUEPRINT

Published 11:03 a.m. UTC April 29, 2024

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy.

Getty Images

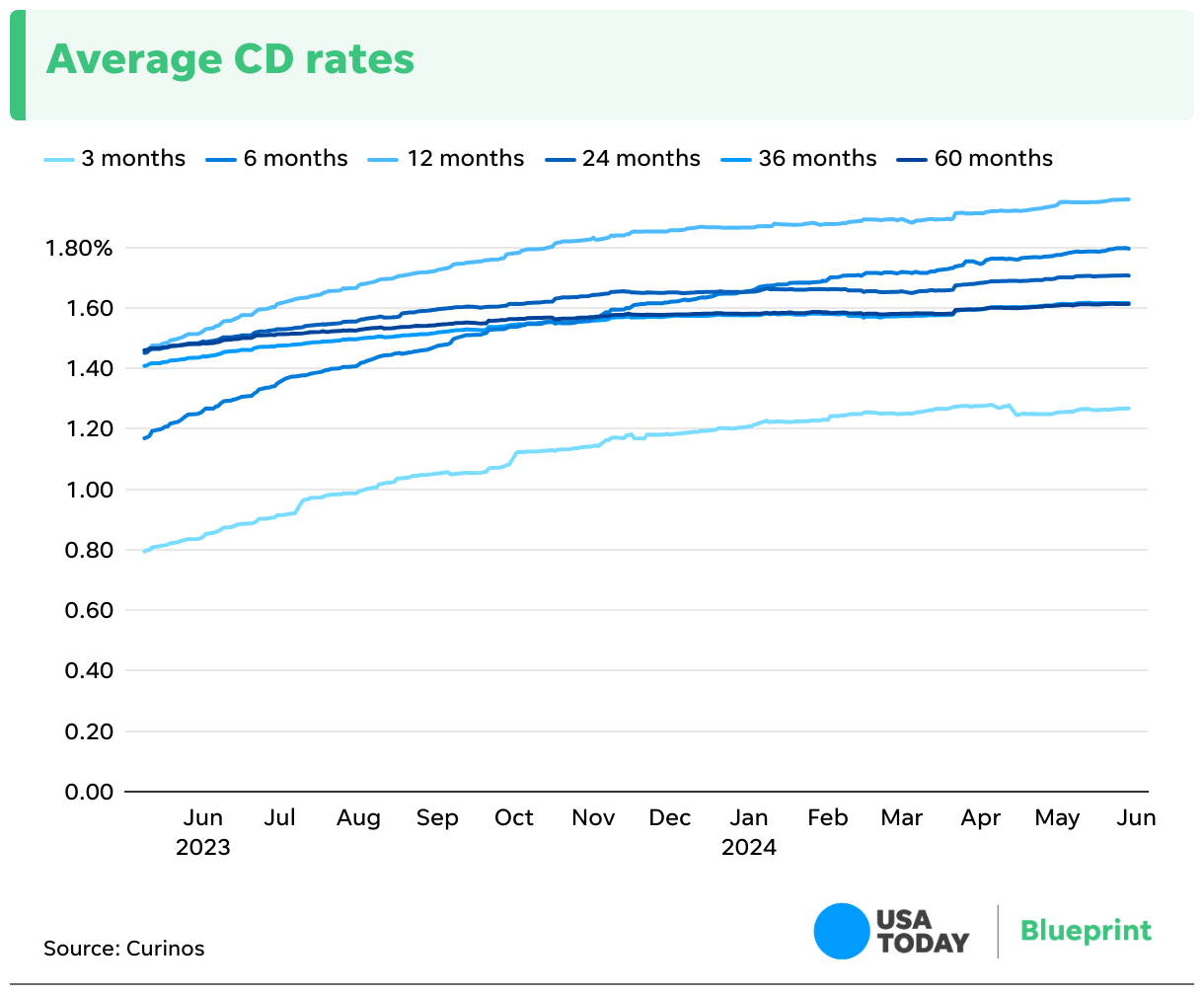

Certificates of deposit (CDs) can be an arrow in your savings quiver, best used to generate good returns on cash you don’t need right away. CD rates have mostly held tight over the past week and remain much higher than last year’s levels. The national average for a 6-month CD with a $25,000 deposit stands at 1.77%, while a 1-year CD currently yields 1.93%. Additionally, 2-year and 3-year CDs offer average rates of 1.70% and 1.61% respectively.

| CD RATES TODAY | ||

|---|---|---|

Term

| Average APY

| High rate

|

3-month CD

| 1.25%

| 5.39%

|

6-month CD

| 1.77%

| 5.45%

|

1-year CD

| 1.93%

| 5.37%

|

2-year CD

| 1.70%

| 5.03%

|

3-year CD

| 1.61%

| 4.85%

|

Source: Curinos. Data accurate as of April 26, 2024. Quoted rates are based on a $25,000 deposit.

| ||

Three-month CD rates

Rates on three-month CDs have remained the same from a week ago. The national average rate was 1.25% as of April 26, 2024, the latest data available, the same as the previous week and down three basis points from a month prior.

The current national high for a three-month CD is 5.39%, which would earn more than $330 in interest with a $25,000 deposit.

Six-month CD rates

The top six-month CDs can offer the best of both worlds: strong interest rates and a short-term commitment.

The national average APY for six-month CDs is 1.77%, the same as last week and up from 1.75% one month ago.

The current top national rate for a 6-month CD is 5.45%, according to the data available from Curinos. But you may be able to find better deals by shopping around.

You’d earn almost $680 in interest if you put $25,000 in a six-month CD with a rate of 5.45%.

One-year CD rates

If you’re up for setting aside your savings for a full year, you’ll be able to pick up even more impressive rates. One-year CDs can give you returns as high as, or even higher than, longer-term options.

Rates on 12-month CDs are increasing. The national average APY is 1.93%, up one basis point from last week and two basis points from a month before.

The current national high for a 12-month CD is 5.37%, which would earn roughly $1,340 in interest with a $25,000 deposit.

Two-year CD rates

Interest rates on CDs with longer terms, such as those spanning two years, are climbing.

The national average APY is 1.70%, a one basis point increase from last week and up two basis points from one month ago.

The current national high for a 24-month CD is 5.03%. By locking in a rate close to this high, you’ll make the most of your returns on this longer-term investment.

If you invest $25,000 in a 24-month CD at the high rate of 5.03%, you’d earn around $2,580 in interest.

Three-year CD rates

The national average APY for a three-year CD stands at 1.61%, which is up one basis point from last week and up two basis points from a month ago.

The highest rate was 4.85%, which would net almost $3,817 in interest if you invested $25,000.

Methodology

To establish average certificate of deposit (CD) rates, Curinos focused on CDs intended for personal use. CDs that fall into specific categories are excluded, including promotional offers, relationship-based rates, private, youth, senior, student/minor, affinity, bump-up, no-penalty, callable, variable, step-up, auto transfer, club, gifts, grandfathered, internet-only and IRA CDs. The average CD rates quoted above are based on a $25,000 deposit.

Frequently asked questions (FAQs)

You’ll need a few key details to open a CD: your name, address, Social Security number, government-issued ID and phone number. You can open a CD online or in person, but you’ll probably find better rates online. Once you get the green light, you can fund the CD with cash from a linked bank account or one that’s not affiliated with the bank at all.

A CD ladder helps you take advantage of higher rates offered by longer terms without tying up your money indefinitely.

For instance, let’s say you have $12,000 to invest and decide to create a ladder of three CDs. You invest $4,000 each into one, two and three-year CDs. When the one-year CD matures, you convert your principal and earned interest to the higher-rate 36-month CD, and do the same with the 24-month CD the next year. This way, you’ll eventually end up with three 36-month CDs with high APYs, with one maturing each year.

Here’s how you can build your own CD ladder:

- Split the amount you want to invest by the number of CD terms you’d like.

- Research the best CDs to find top providers and the best rates for various lengths.

- Set up the CD accounts you’ve chosen.

- As the CDs mature, reinvest the cash into longer-term CDs.

The second step is crucial. Just because the Fed has raised interest rates doesn’t mean you’ll get the same or even similar rates from different financial institutions for the same CD term.

A basis point is the term used to describe one hundredth of one percentage point. Therefore, if the yield on a CD increased from 1.50% to 1.60%, it increased by 10 basis points.

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.