Today’s top savings account rate roundup: Earn up to 5.84% — April 29, 2024

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

BLUEPRINT

Published 11:11 a.m. UTC April 29, 2024

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy.

Getty Images

Savings account rates have held firm over the past week, though savers can earn much higher yields now compared to this time last year. This is a positive development, to be sure, but make sure you consider fees, customer service and user-friendly digital experience when selecting a savings account.

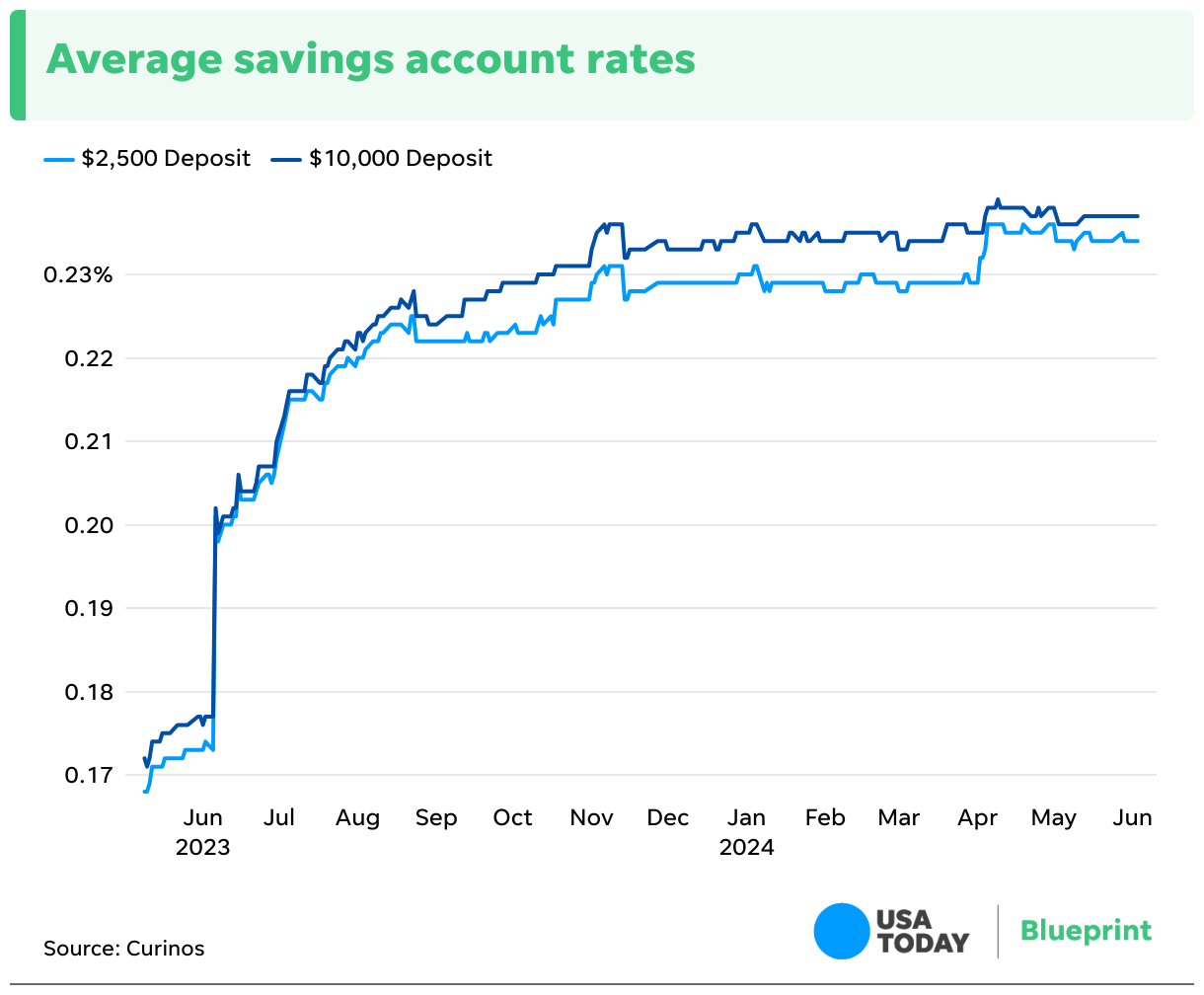

| SAVING RATES TODAY | ||

|---|---|---|

Average APY

| High rate

| |

$2,500 minimum deposit

| 0.24%

| 5.84%

|

$10,000 minimum deposit

| 0.24%

| 5.35%

|

Source: Curinos. Average APY accurate as of April 26, 2024.

| ||

Commonly referred to as “statement savings accounts” in the banking world, savings accounts paid negligible yields after the Great Recession. The Fed maintained low borrowing costs for several years in order to bolster economic growth.

The landscape, however, became topsy-turvy after the government’s extensive spending during the pandemic. The Fed belatedly countered by increasing interest rates at an unprecedented pace in order to offset soaring inflation, prompting banks to raise rates for savers.

Savings account rates — $2,500 minimum deposit

The highest interest rate on a standard savings account today is 5.84%, per Curinos, the same as a week ago. Meanwhile, the average APY (annual percentage yield) for a traditional savings account, as reported by Curinos, is 0.24%, up slightly from last week.

APY represents the return your account will generate in a year, taking into account compound interest—the interest earned on both the principal and previously accumulated interest in your account.

For instance, if you were to invest $2,500 at a 5.84% rate (the current high) for one year, you would earn around $150 in interest, assuming daily compounding and no additional contributions.

Savings account rates — $10,000 minimum deposit

The average APY for savings accounts requiring a minimum deposit of $10,000 is 0.24%, unmoved over the past week. But remember that many banks offer substantially higher rates.

Some of the top high-yield savings accounts, for instance, currently feature rates of 4.00% or higher.

Per Curinos, the highest interest rate today on a savings account requiring a minimum deposit of $10,000 is 5.35%. If you were to invest $10,000 at a 5.35% rate (the current high) for one year, you would earn more than $550 in interest, assuming daily compounding and no additional contributions.

Methodology

To establish average savings account rates, Curinos focused on savings accounts intended for personal use. Savings accounts that fall into specific categories are excluded, including promotional offers, relationship-based accounts, private, youth, senior and student/minor. The average savings rates quoted above are based on a $2,500 or $10,000 minimum deposit amount.

Frequently asked questions (FAQs)

A high-yield savings account is ideal for those who require a readily accessible option for funds that won’t be touched more than once a week. It’s a recommended choice for most people.

However, if you already have a well-balanced investment portfolio with high earning potential and a convenient savings account with a trusted bank, you might not need or want a high-yield savings account. In this situation, managing an additional account could be an unnecessary hassle.

A savings account offers a secure space for you to store money that isn’t required for daily use. Keeping savings separate from your everyday funds can help reduce the temptation to spend impulsively.

A savings account can act as a rainy-day fund, earning interest while maintaining liquidity.

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.